GuruScreens - upgrades and downgrades - October 21st

The FTSE is still struggling against the backdrop of uncertainty in the Eurozone. Indeed, the FTSE 100 closed at 6195 last Thursday - its lowest point since June 2013. Some GuruScreens will inevitably hold up better than others in these circumstances. This week we take a deeper look by analysing companies that have passed through three respective income, growth and momentum screens.

Winning Growth & Income

The Winning Growth & Income Screen searches for companies with good growth credentials that offer above average dividend yields. It is interesting to note that companies which qualify for this screen must have a Beta below 1 - meaning that the stock price must be less volatile than the market. Stocks with a lower Beta have historically tended to decline more slowly during a bearish phase. In the UK for example, the FTSE 100 has fallen by 7% over the last 3 months, while the Winning Growth & Income Screen has only dropped 2.3%. Let’s take a look at the companies that have passed through this screen.

Pennant International

Pennant International (PEN) qualified for the screen on the 1st October. The firm provides and supports training software systems to military and civilian customers, based on emulation, simulation and virtual reality. For example, they provide the UK MoD with virtual reality parachute training systems.

The yield is 3.35% on a TTM basis, while brokers expect the company to pay a 3.85% yield in 2015. There were some red flags over the firm’s cash flow in 2013. The company reported operating cash flows (0.62p per share) that were well below earnings (6.33p per share). If a company has bad cashflow but attempts to maintain its dividend, it may be financing the payout with debt. However, on a TTM basis, Pennant’s operating cash flows have risen to 7.95p per share, while the company generated 6.47p in terms of earnings per share.

The company has managed to generate these earnings and cashflows partly by securing a string of new contracts. Pennant’s final year report for 2013 noted that “Record new orders [were] taken during the year worth in excess of £20m”. Indeed, Pennant won its largest ever contract - worth £16m over 5 years to supply and support a suite of training aids to the Australian Defence Force. The company also has a high StockRank of 92. Is share price has beaten the market by 17% this year and it has a ROCE that is higher than 94% of UK listed companies. However, it still trades on a relatively low PE ratio (12.4).

Jim Slater Zulu Screen

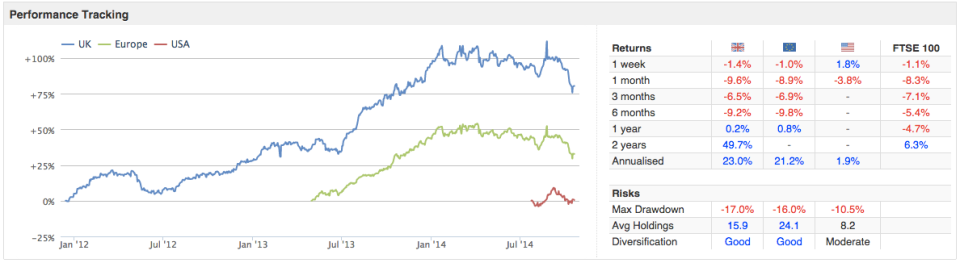

Stockopedia’s Zulu Principle Screen is inspired by Jim Slater’s bestselling Zulu Principle book. The screen uses a combination of growth and value metrics, looking for shares where brokers are forecasting high earnings growth, but which are currently valued at a price that is low relative to their forecast earnings. The screen has returned nearly 50% over the last two years, while the FTSE 100 has only appreciated by 6.3%.

However, the screen has actually underperformed the market over the last month or so. During the past two years it has tended to do very well in bullish phases, but has come down harder when the bear market strikes. This is partly because it uses forecasts growth rates extensively in the calculation of the PEG, PE and EPS Growth metrics. It may therefore become vulnerable in market environments where brokers are reducing estimates.

Thorntons

Over the last few years Thorntons (THT) has succeeded in growing earnings partly by closing its own high street stores, while continuing to sell in large volumes through its Fast Moving Consumer Goods Division. Brokers expect the company to continue growing earnings by around 18% over the next twelve months. However, the company’s sales fell by 12% in the first quarter and the company now trades on a forecast PE ratio of 9.5. This gives the company a PEG ratio of 0.6.

This will be an interesting one to watch. Cost-cutting was an important factor that helped the company grow profits, but can a company keep cuttings costs forever? Thorntons’ management team expect to see ‘year on year UK Commercial sales growth’ going forward, ‘albeit at a more modest level due to strong prior year comparatives.’

Price Momentum Screen

As the name suggests, the Price Momentum screen looks for stocks that have recently been rising in price. To qualify for it, a company must have beaten the market over the previous 1 month, 6 months and 12 months periods. The screen has come down quite heavily in recent months, partly because momentum tends to suffer sharp reversals during a bear market. However, we never know where we are in the bull-bear cycle, so it is worth taking a look at companies from a wide range of strategies.

Hutchison China Meditech

Hutchison China Meditech (HCM) is engaged in the research, development, manufacturing and sales of pharmaceuticals, health supplements and other consumer health and personal care products. The company enjoys favourable tailwinds in China, namely rising government spending on healthcare, rising living standards, and favourable demographic trends. It is also well placed to drive expansion through the sale of properties, which have appreciated in value in line with rising land prices.

This may help to explain why the company has beaten the market by an impressive 83% over the last year and nearly 20% over the last 3 months. The company also trades 23% above its 200 day moving average. That being said, it trades on an extremely high PE ratio 128, so the company has a very long way to fall if anything does go wrong.

Read More about Thorntons on Stockopedia

Discuss Thorntons on Stockopedia