US 10-Year Treasury Yield Jumps To 3%

Bonds generally had another poor week as yields rose across the board, hurting the performance of fixed income funds. The US 10-year yield spiked to the highest level since July 2011, weighing on the performance of longer-dated bonds. Over the week ended 6 September 2013, global bonds saw a hefty 12.4bps spike in yields to 2.659%, while G7 sovereign bonds saw a similar 8.3bps rise in yields. US investment-grade corporate bonds saw a fairly large 12.9bps increase in yields to 4.23%, while within the riskier segments of fixed income, hard currency EM bonds saw a further 3.4bps increase in yields to 6.037%.

Boosted by the Australia dollar 3.61% weekly gain against Malaysia ringgit, Hwang AUD Income Fund rallied 3.64% and became the top performing fixed income fund last week. AmDynamic Bond and AmTactical Bond declined -0.78% and -1.15% respectively due to their exposure on the underperforming Indonesia bonds. On average, 17 Malaysia pure bond funds returned -0.03% last week.

GLOBAL BOND MARKET

Major central banks which held monetary policy meetings over the week included the European Central Bank, the Bank of England, the Reserve Bank of Australia as well as the Bank of Japan – not surprisingly, all kept their benchmark rates unchanged, although investors were eagerly screening policy statement announcements for hints on the future direction of monetary policy. The European Central Bank (ECB) showed its lack of enthusiasm over improvements seen across various Eurozone leading indicators, holding its monetary policy unchanged whilst emphasising a bias towards keeping interest rates low as long as there is an “overall subdued outlook for inflation”. Displaying much caution, ECB President Mario Draghi was quick to highlight that the recovery still remains in its infancy, with risks to the downside for Europe.

Within the emerging markets, central banks of Malaysia, Mexico and Poland met over the week, with Malaysia and Poland holding their benchmark rates steady, while Mexico surprised markets with a 25bps cut in the benchmark overnight rate to a record-low 3.75%, the second rate cut this year. This comes on the back of growth concerns in Mexico (on muted exports to the US), and is in stark contrast to the rate hikes undertaken by emerging markets like India and Indonesia in efforts to stem capital outflows which have appreciably weakened their currencies so far in 2013.

In the US, a stronger-than-expected surge in PMIs for both the services and manufacturing sectors coupled with an upward-revision to 2Q 13 GDP growth (2.5% on a quarter-on-quarter annualised basis, up from 2.2% in the advance estimate) sent longer-dated Treasury yields higher over the week as Fed “tapering” fears intensified, with the 10-year US Treasury yield crossing the 3% mark on 6 September, the highest level reached since July 2011. With short-term rates anchored by the Fed Funds rate, the spread between longer and shorter rates has increased to historically-wide levels; along with muted inflationary expectations, this may hint at some reversal in the direction of longer-dated yields in the near-term, particularly if tapering fears begin to subside.

We remain cognisant of the risks of rising interest rates, and continue to urge investors to avoid longer-duration developed sovereign debt which are the most susceptible to rising yields. Given that Malaysia bonds generally have higher yields compared to developed market bonds (due to the country’s “Emerging Market” status), rising global yields are less likely to have a significant impact on the domestic bond market.

MALAYSIA BOND MARKET

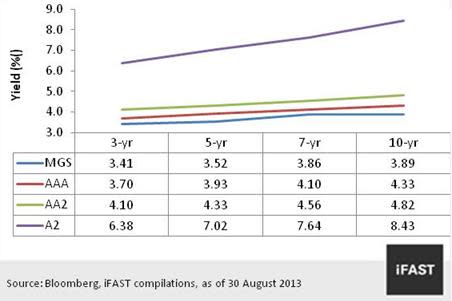

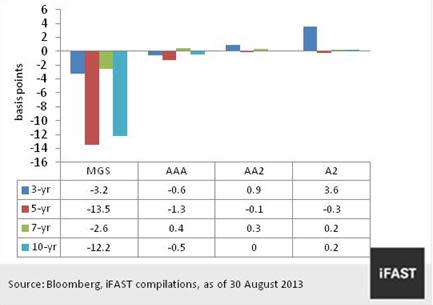

The yields on Malaysia Government Securities were traded lower by -2.5bps to -13.5bps last week as the fuel subsidy reduction and stable overnight policy rate decision added some positives on the government to strengthen its fiscal position. Besides, market players are awaiting more measures to be unveiled in Budget 2014 on 25 October 2013 which will paint the macroeconomic picture in near to medium term. As of 6 September 2013, the yields on 3, 5, 7 and 10 years MGS were closed at 3.41%, 3.52%, 3.86% and 3.89%. On the government bonds’ auction side, the government will put 5 years, 7.5 years and 30-years bonds on sales in the month of September.

The average trading volume on local corporate bonds climbed 33.5% to RM511 million last week with AAA-rated and AA-rated corporate bonds each commanded 47% of the total trading activities. Within the local corporate bonds segment, AAA-rated Malaysia Airport Holdings Berhad bonds (4.15% MAHB IMTN due 2018 and 3.85% MAHB IMTN due 2016) were traded actively with 20 trades worth of RM330 million recorded last week.

On local credit ratings action front, RAM Ratings commented that the lawsuit against Fraser & Neave Holdings Berhad will not have any significant impact on the issuer’s RM1 billion MTN credit ratings. MARC has placed negative outlook on the AA-rated Maju Expressway Sdn Bhd’s RM550 million IMTN due to the concern on the potential increase in its financial leverage and it might be under pressure from its parent company to return surplus cash to the shareholders.

Visit Fundsupermart.com website for more articles on markets and unit trusts.